Featured

Table of Contents

It attempts to lower the interest paid on that debt to around 8%, sometimes lower. The regular monthly payment is sent to a nonprofit credit therapy firm, distributing an agreed-upon total up to each card company. The goal of debt management programs is to be the go-between for consumers searching for a way to remove debt and credit card business who wish to earn money what they are owed.

That generally involves a substantial concession on rates of interest by the card companies in return for the pledge that the consumer will pay off the debt in a 3-5 year duration. Financial obligation management programs are not a loan. Those come from banks or cooperative credit union. Financial obligation management programs do not guarantee to decrease the quantity owed.

The simplest method to enroll in a financial obligation management program is to call a not-for-profit credit counseling agency, ideally certified by the National Foundation for Credit Counseling (NFCC). You can find a list of nonprofit credit counseling agencies by typing debt management program into a search engine, however a word of caution: Make sure the action you choose is a nonprofit credit therapy firm and NOT a debt settlement business.

Required Mortgage and Financial Counseling in 2026

When you call a not-for-profit agency, be prepared to answer concerns about your income and expenditures from a licensed credit counselor. The more information you have about these two locations, the simpler it will be for the counselors to offer a service to the problem. Before speaking with a credit counselor, it might be in your benefit to take a look at your credit report (which you can secure free from ), so you have an accurate image of who you owe and just how much you owe.

If you do not get approved for a financial obligation management program significance you don't have adequate income to handle your costs counselors will direct you toward another service, which might be financial obligation settlement or bankruptcy. Not everybody certifies for a debt management program. If you discuss your budget plan with a therapist and there isn't cash offered to manage expenses, the counselor ought to recommend you that financial obligation management will not work.: The therapist might determine that you have actually simply been reckless about spending and can get rid of the debt yourself by doing a much better task with budgeting.

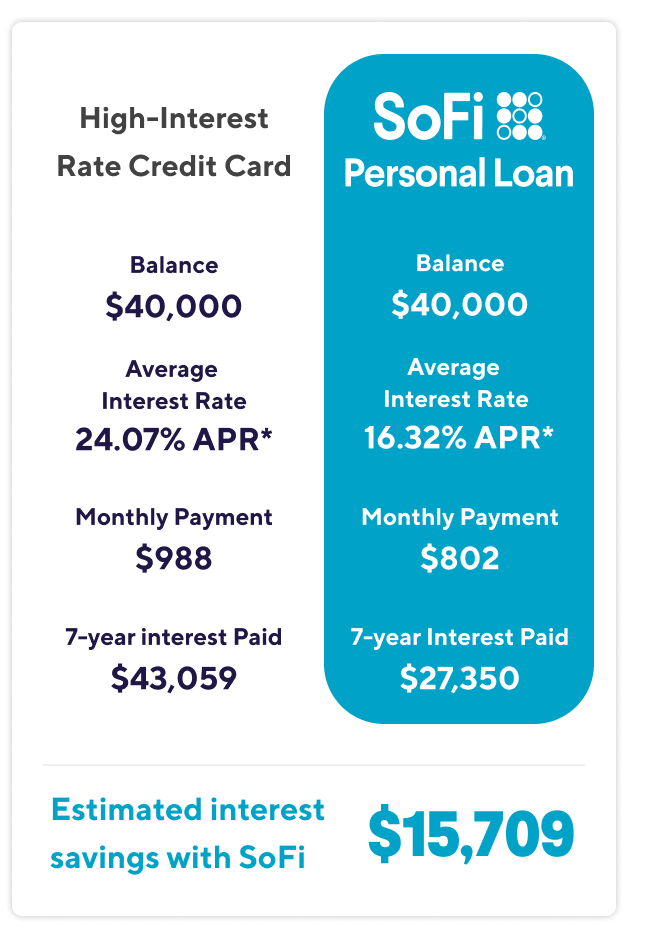

This program lets you repay less than you owe, but your credit rating will tank, and you may accumulate late fees during the negotiations with your lenders. This method frequently includes getting a loan at a lower rate of interest to settle unsecured debt. It normally takes a decent credit history to qualify, but the procedure is quickly, and funds can hit your account a day after using.

Expert Financial Relief Plan Evaluations in 2026

If you disagree with the option used, ask why that is the very best choice, or contact another therapy agency and see if they agree.

American households are carrying a few of the greatest financial obligation levels on record. In mid-2025, charge card balances passed $1.21 trillion, and the average cardholder owed more than $6,300. With purchase APRs now averaging about 22%, lots of households find that even paying the minimum each month barely damages their balances. Increasing delinquencies demonstrate how challenging it has actually ended up being to maintain.

The Necessary Guide to 2026 Debt Combination for New York City Debt Management Program HouseholdsThese companies negotiate with creditors to minimize the overall quantity owed on unsecured debts like credit cards or individual loans. While settlement can lower balances, it's not without tradeoffs credit scores can be impacted, and taxes may apply on forgiven financial obligation.

We limited this list to companies that concentrate on financial obligation settlement programs where arbitrators deal with lenders to lower the total quantity you owe on unsecured debts. Business that just offer loans or credit counseling strategies were not consisted of. The following aspects guided our rankings: Market accreditation: Confirmed subscription with groups such as the American Association for Financial Obligation Resolution (AADR) or the Association for Customer Debt Relief (ACDR). Cost structure: Programs that follow FTC guidelines and charge no upfront costs, with expenses gathered only after a settlement is reached and a payment is made.

Accessing Statewide Relief Assistance Resources in 2026

State schedule: How many states the business serves. Minimum financial obligation requirement: The lowest quantity of unsecured financial obligation required to register, frequently $7,500 or $10,000. Track record and scale: Years in operation, number of accounts resolved and acknowledgment in independent rankings.

Founded in 2009, it has actually turned into one of the biggest and most recognized debt settlement companies in the nation. The business is an accredited member of the Association for Consumer Debt Relief, which signals compliance with market requirements. Scale sets National Debt Relief apart. It works with more than 10,000 lenders, fixes over 100,000 accounts every month, and has actually settled nearly 4 million debts given that its launch.

National Debt Relief charges no upfront costs. Customers pay a fee usually in between 15% and 25% of the enrolled financial obligation just after a settlement is reached and a payment is made. Programs are generally offered to individuals with a minimum of $7,500 in unsecured financial obligation, and services encompass 46 states, more than some competitors.

1 Accomplish ranks 2nd for 2026. Founded in 2002, Achieve runs as part of Achieve Financial, a more comprehensive monetary services business that also provides personal loans and credit-building tools. Its financial obligation settlement services focus on negotiating unsecured debts such as charge card and individual loans. Accomplish generally needs a minimum of about $7,500 in unsecured debt to register.

Ways to Combine High-Interest Debt in 2026

Costs generally fall within the market variety of 15% to 25% and are just gathered after a settlement is reached and a payment is made. Clients can evaluate and approve each settlement before it is finalized. Attain sticks out for its long operating history and structured client tools. While financial obligation settlement is one part of a larger product lineup, the company has made strong customer reviews and maintains clear disclosures about costs and process.

For customers who value an established company with incorporated financial tools and transparent settlement practices, Achieve is a strong competitor. 2 Founded in 2008, Americor is a financial obligation relief business that focuses on financial obligation settlement for unsecured financial obligations such as credit cards and personal loans. The company is a member of the American Association for Debt Resolution, which shows adherence to market requirements.

{kind=link}

Latest Posts

Using Loan Calculators for 2026

Essential 2026 Planning Calculators for Borrowers

Key Queries About Professional Debt Relief in 2026